January 2022

Housing Market Outlook in 2022 according to NAR

The National Association of Realtors expects the economy to expand at a modest rate of 2.6% in 2022 as the Federal Reserve Board tightens monetary conditions to rein in inflation towards a long-run average of 2%.

The 30-year fixed mortgage rate is expected to increase to an average of 3.5% in 2022 from 3% in 2021. However, it is worth emphasizing that the 3.5% rate is still low by historical standards and is lower than the average rate of 3.9% in 2019. With higher mortgage rates, existing-home sales are expected to decrease slightly to 5.9 million in 2022.

Supply chain bottlenecks are expected to ease in 2022, barring a major resurgence of a COVID variant (Delta, Omicron). However, the labor market will continue to tighten, with the unemployment rate falling further to an average of 4.9%. Under these conditions, total new housing units started (single-family and multi-family) are expected to only modestly increase to 1.67 million. Housing starts will be at pace with household formation (1.75 million in 2020).

Given the modest increase in housing supply, home prices are expected to continue to increase, although at a modest pace of below 5%. Strong employment growth, relatively affordable housing prices, and good infrastructure, including broadband access, will continue to drive the difference in local market housing conditions.

The National Association of REALTORS® is America's largest trade association, representing more than 1.5 million members, including NAR's institutes, societies, and councils, involved in all aspects of the real estate industry.

Top 10 Undervalued Markets in 2021

The National Association of REALTORS® identified top 10 markets that underperformed in 2021 relative to their underlying market fundamentals. These markets are expected to experience stronger price appreciation relative to other markets in 2022.

What is an undervalued market? NAR considered a market undervalued if its median home price-to-median family income ratio is at the lower end of the distribution of 379 metro areas relative to the distribution of a combined set of seven indicators that drive demand and supply:

Those 10 markets were Dallas-Fort Worth, TX; Daphne-Fairhope-Farley, AL; Fayetteville-Springdale-Rogers, AR-MO; Huntsville, AL; Knoxville, TN; Palm Bay-Melbourne-Titusville, FL; Pensacola-Ferry Pass-Brent, FL; San Antonio-New Braunfels, TX; Spartanburg, SC; Tucson, AZ.

Bay Area ZIP codes with the fastest home price growth

According to the San Francisco chronicle, homes in more suburban and rural ZIP codes of the Bay Area had the biggest price growth jump from Dec. 2020 to Nov. 2021, while homes in city center ZIP codes had the smallest price increases, according to Zillow.

By ZIP code, the area with the biggest increase of 38% was Sea Ranch, a small, remote community on the Sonoma County coast with Bolinas, another seaside town in Marin County, coming in second at 28%. A third waterfront community, Bethel Island in Contra Costa County, had the third highest home value increase of 27%. Other locations were Union City, Pleasanton, San Ramon, Dublin, Oakley, and Livermore.

Homeowners Experience Sticker Shock on Insurance Premiums

Homeowners who are renewing their home insurance policies are finding their rates are drastically climbing. Insurance companies point to rising material costs and climate change as the main reasons behind the increases.

Premiums are up, on average, by 4%. The average annual homeowner insurance premium is $1,398, according to the Insurance Information Institute, known as Triple-I. Since 2017, premium rates are up 11.4%. That is faster than inflation, The Washington Post reports. Insurance companies say homeowners should brace themselves for further rises.

New Housing Fails to make up for Decades of Undersupply

Recently released census data provides another measure to illustrate how California is not providing enough housing to shelter its population. The Public Policy Institute cites data provided by the 2020 Census, which includes a full accounting of the nation's housing stock.

By this measure, California's new housing has fallen short of population growth. Specifically, the state added 3.2 times more people than it did housing units over the last 10 years. There are now 2.93 Californians for every occupied housing unit, behind only Utah (3.09) and Hawaii (2.93), and far above the average of all other states (2.53).

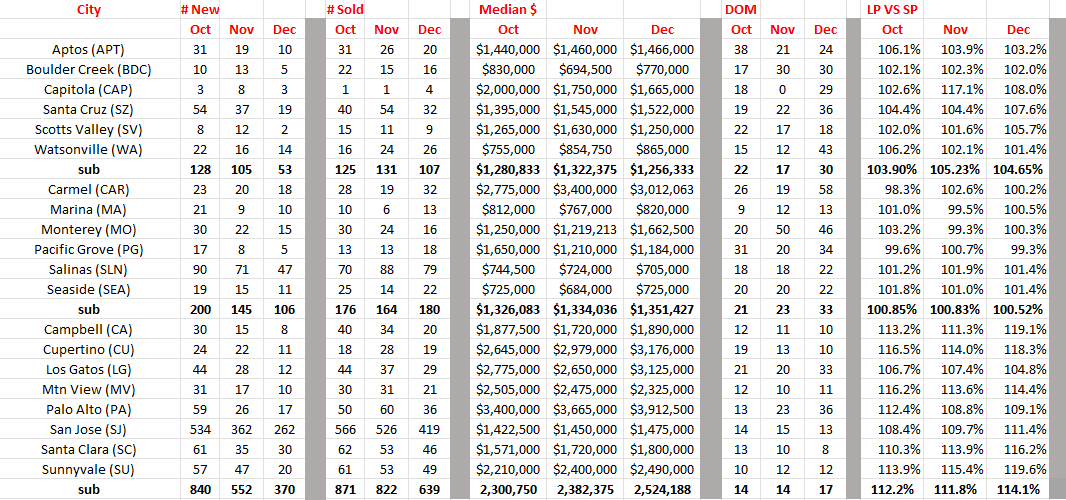

Fourth Quarter Stats for Santa Cruz, Monterey & the Bay Area

Comments: Obviously, new listings dropped substantially over the final months of the year as normal. I will do an annual comparison next month. Sales in December were almost double new listings. Lack of inventory drives the market especially when new listings decline. Prices didn't move much except in Santa Clara County. Days on the market increased a bit due to the holidays, I would imagine. List price to sale price only increased in Santa Clara County. Display of MLS data is deemed reliable but is not guaranteed accurate by the MLS.

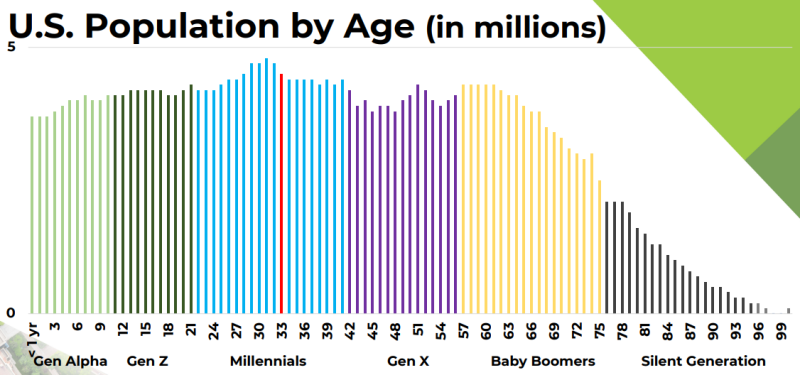

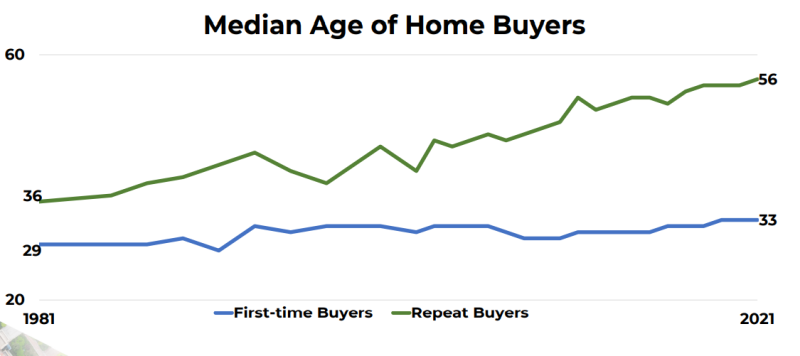

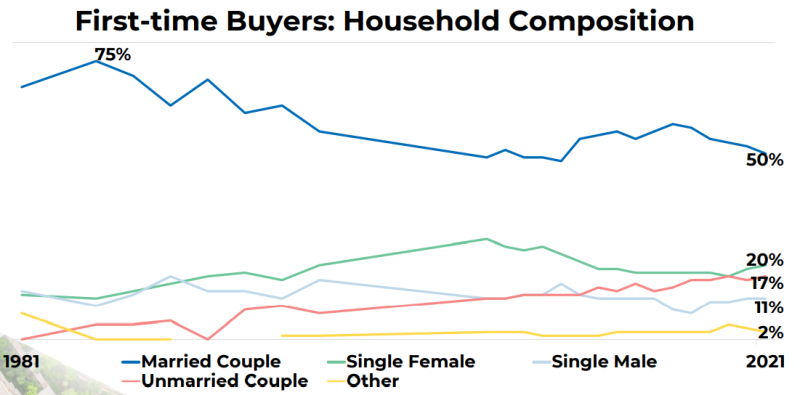

Home Buyers, Sellers and Demographics for year ending 2021