DECEMBER 2023

Existing home sales are likely to rise in 2024

According to Housing Wire, higher mortgage rates and high home prices reduced the number of sales of existing homes down 4.1 percent in October compared to September, and down 14.6 percent compared to a year ago, according to the NATIONAL ASSOCIATION OF REALTORS®. These conditions proved difficult for prospective home buyers, especially for first-time buyers. However, conditions were good for home sellers.

Experts expect interest rates to decline somewhat in 2024 and home builders to have more homes ready for purchase. Inventory rose 1.8 percent in September, with 1.15 million units on the market, and after the holiday season, experts expect the market to pick back up.

If you want to know what is happening in Santa Cruz County, be prepared as sales for 2023 will most likely not reach one-half of what they were in 2022. See the stats since 1980 here. It actually may be the lowest year on record for sales of single-family homes in the last 20 years.

FHFA announces 2024 conforming loan limits.

The Federal Housing Finance Agency (FHFA) announced it will increase the 2024 conforming loan limits for mortgages acquired by Fannie Mae and Freddie Mac to $766,550 on one-unit properties and a cap of $1,149,825, in high-cost areas (this applies to the Bay Area). The previous loan limits were $726,200 and $1,089,300, respectively.

C.A.R. and N.A.R. both have long advocated for loan limits that reflect an area's cost of housing. As a result of C.A.R.'s and N.A.R.'s efforts, areas with high median home prices have benefited from a loan limit above the national conforming loan limit. The conforming loan limit determines the maximum size of a mortgage that government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac can buy or "guarantee."

Home prices expected to soar in these California cities.

With mortgage rates finally easing, many California cities are expected to see home sales rebound significantly next year, according to a forecast from Realtor.com. Five metro areas are predicted to see double-digit sales growth in 2024 compared to 2023. Those cities include Oxnard-Thousand Oaks (18 percent), Riverside-San Bernadino-Ontario (13.8 percent), Bakersfield (13.4 percent), San Diego-Chula Vista-Carlsbad (11 percent) and Sacramento (10.3 percent).

Home sales in the Los Angeles-Long Beach area are expected to climb 9.2 percent after two years of declining sales. Sales in the San Francisco-Oakland-Berkeley area are expected to stay flat, while sales are expected to decline 18.5 percent in San Jose-Sunnyvale-Santa Clara and 6 percent in Fresno. In addition, home prices are predicted to fall in some areas, according to the forecast. Home prices in San Diego are predicted to fall approximately 5.2 percent in the next year, and in Stockton by about 3.7 percent.

Beware of 'Title Pirates' wreaking havoc on closings

Fraudulent real estate sales are on the rise. The FBI's Internet Crime Complaint Center warns that losses from real estate and rental scams are steadily increasing, reaching more than $396 million last year.

Victor Petrescu, an attorney with Levine Kellogg Lehman Schneider + Grossman LLP in Miami who represents victims of real estate scams, says he's noticing an uptick in one particular type of scheme: title fraud. "Pirates," as he calls them, are recording fake liens or deeds that are jeopardizing a growing number of closings and putting more homeowners at risk.

What is a "title pirate"?

It's a term that refers to a person or entity who commits title fraud by attempting to create the appearance that the person or entity has legal title to a piece of real property when they do not.

To accomplish this, a title pirate will usually use falsified documents, such as a forged driver's license or Social Security card, to hold themselves out as the owner of a parcel of property. Title pirates can then profit by, among other things, securing a loan on the property, renting the property out, temporarily living in the property or attempting to sell the property to a potential buyer.

How common is this scam?

Title piracy has become increasingly more common since 2020, especially with the rise of remote and mail-away closings and remote notarization in our post-COVID society. It has been an especially big issue in South Florida in recent years.

Who do title pirates tend to target?

Title fraud can take many forms. Vacant parcels of land are a favorite target among title pirates because they are not occupied, and they are not usually closely monitored by their actual title owner, who may even be located out of state. In the case of vacant properties, once a title pirate records documents purporting to grant them an interest in the title, their next step is usually to attempt to borrow money against the property from third-party lenders. This is usually based on the title pirate's representations that the money will be used as a construction loan to finance construction on the property. Then, subsequently, they'll abscond with the funds after the loan's closing without paying the lender back afterward, leaving the lender to attempt to foreclose their loan against a property the borrower does not have legal title.

Properties with recently deceased owners and investment properties owned by holding companies are another potential target. As an example, in May of 2018, the Broward County Sheriff's Office in Florida arrested a group of people who, using forged quit claim deeds and powers of attorney, purported to take the title of 44 homes in Broward County that the group did not actually own. Eighteen of those were owned by the estates of deceased owners. The group would rent the homes, attempt to sell them, or even live in them.

What should you do if you become a victim of a title pirate scam?

You should immediately contact a lawyer to discuss the most efficient and expedient way for you to clear your chain of title. If you have title insurance, you should also initiate a claim with your title insurance carrier. You should also contact your county clerk's recorder's office to notify them of the fraud.

Should you buy a Home Warranty?

Who knew people were so fervent about home warranties! Everyone has their own experience; expect to hear a few people call them "a scam" or at the very least a waste of money. Others will regale you with their tale of how having a warranty saved them from a freeing winter because they couldn't afford to fix their furnace without it.

In the end, the decision is personal and largely based on how comfortable you are coming out of pocket if one of the more expensive items in your home, like the air conditioning unit or hot water heater, should malfunction and need to be replaced. We're breaking down three important particulars so you can make an educated decision.

Know the cost.

"A basic home warranty costs about $350 to $500 a year or more," said Money Talks News. "A warranty typically covers kitchen appliances, plumbing, water heater, heating and electrical system components, sump pump, whirlpool tub, and ceiling and exhaust fans, according to Angie's List. "'Enhanced' plans, purchased for another $100 to $300, provide added coverage for such things as a washer and dryer, air conditioning system, refrigerator, and garage door opener. Optional coverage can be added, including for pools and septic systems."

You can typically break down the annual cost into monthly payments if that's more comfortable for you, but the cost of the warranty itself isn't the only thing you're responsible for paying. Service calls will typically also cost you; put in a work order for a broken microwave or a tub that won't drain and you'll be responsible for paying for the privilege of having a professional come check it out, and hopefully fix it.

"Home warranty deductible, or service call fees, is an important concept to master if you want to understand how to find the cheapest home warranty plans for your needs," said Review Home Warranties. With most home warranties, a deductible or service call fee will be required, "with an industry average of approximately $75 per visit. Some companies, like American Home Shield or Total Protect Home Warranty, let their customers choose the amount of a deductible, which depends on the amount of premium. The higher the premium, the lower the deductible."

Consider your peace of mind!

Many homeowners opt for a home warranty for major "just-in-case" scenarios. Just in case the air conditioning unit crashes and burns. Just in case the hot water heater dies. Just in case there's some other expensive repair that pops up, without the ability to comfortably pay for it. With the cost of some of these items running into the thousands average for a new air conditioning unit and installation, per HomeAdvisor, is $5,413!-the peace of mind factor is huge.

"For a homeowner who doesn't have an emergency fund or who wants to protect their emergency fund, a home warranty can act as a buffer," said Investopedia. "Home warranties also make sense for people who aren't handy or who don't want to worry about tracking down a contractor when they have a problem. Warranties can also make sense for people with expensive taste in appliances."

But...understand that not everything is covered.

There's always a chance that the item you need repaired is not covered under your warranty for one reason or another. "Having a home warranty doesn't mean the homeowner will never have to spend a penny on home repairs," said Investopedia. "Some problems won't be covered by the warranty, whether because the homeowner didn't purchase coverage for that item or because the warranty company doesn't offer coverage for that item. Also, home warranties usually don't cover components that haven't been properly maintained. Furthermore, if the warranty company denies a claim, the homeowner will still have to pay the service fee and will also be responsible for repair costs."

In our case, limitations spelled out in our home warranty contract regarding the replacement of outdated parts and refrigerant costs for our broken air conditioning unit meant we had to come out of pocket for $1,500. The lesson here: Read the fine print so you're prepared. FYI: I always buy a home warranty for my buyers when purchasing a new home. I have found that the first year is the most important and it is great to be covered after such an initial first expense in buying a home.

Carbon Monoxide: Preventing a Silent Danger

Carbon monoxide (CO) is an odorless, colorless gas produced by the combustion of fuels such as natural gas, oil, and propane in devices including furnaces, water heaters, and stoves. These appliances are designed to vent the CO to the outside, but improper installation, incomplete combustion of fuel, or blockages, leaks or cracks in venting systems can cause CO to reach harmful levels inside the home. Dangerously high levels of CO can lead to incapacitation or death, with victims sometimes never having been aware they were being poisoned.

Prevention and working alarms are key to avoiding carbon monoxide poisoning:

Learn what to do if the CO alarm activates. If anyone in the home experiences symptoms such as fatigue, dizziness, blurred vision, nausea, or confusion, everyone should leave immediately and seek medical attention. If no symptoms are felt, open doors and windows immediately and shut off all fuel-burning devices that may be potential sources of CO. Keep your family safe and avoid an unnecessary tragedy.

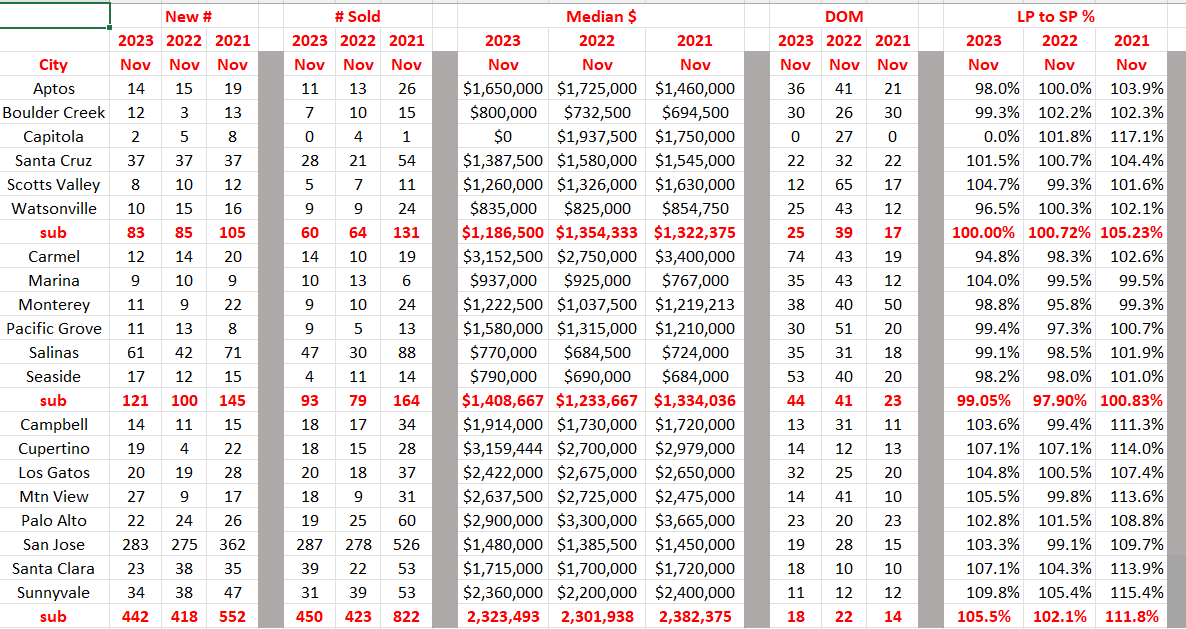

3-Yr November comparison for Santa Cruz, Monterey & the Bay Area

Comments: Comparing last month's stats to this month they are relatively close. I thought it might be interesting to focus on a particular area, such as Santa Cruz. New listings mirrored each other year over year (hmmm). BUT sales declined 62% (2021 to 2022), then grew 25% in 2023, and yet still 49% below 2021. The median price is the indicator everyone looks at with a 13% decline from 2022 and list-to-sales price down 3% as well. Santa Cruz is an area of lower average income compared to the rest of the Bay Area, and workforce housing is unaffordable and scarce leaving the area because of it. In Monterey County, it may be Seaside that we look at. This is an area that has had a 14% increase in median sales price since 2021. Is it because many subdivisions and new homes are being built? And the median price is 44% lower than in Santa Cruz. In Santa Clara County, we look at Palo Alto. The predominantly highest-priced city in the Bay Area. Similar to Santa Cruz, new listings are level and sales significantly lower. The median price is down 21% since 2021 and list to sale price ratio also declining 6%. Has the upper end peaked? What do you think?? (Display of MLS data is deemed reliable but is not guaranteed accurate by the MLS as of 11/30/23)