DECEMBER 2024

Homeowners' wealth jumped $150,000 in 5 years

Though the housing market has been a rollercoaster ride over the past few years, homeowner wealth has surged by nearly $150,000 in the last five years, according to Money.com. The pandemic initially caused a slowdown, but it was followed by a period of unprecedented demand, leading to sharp price increases and a competitive landscape for buyers. According to the National Association of REALTORS®, the pace of price increases has slowed down somewhat, however. The national median home price increased by 3.1% year-on-year in the third quarter of 2024, a slowdown from the 5 percent increase seen in the second quarter. While prices are still elevated, the deceleration suggests a potential shift toward a more balanced market.

NAR's data shows that nearly 90% of major U.S. metro areas saw home price increases in the third quarter of 2024. Prior to 2024, mortgage rates had been steadily rising, reaching a peak above 7%, which had a chilling effect on affordability. However, the 30-year fixed-rate mortgage has since averaged in the mid-6 percent range, improving affordability. The monthly mortgage payment on a typical existing single-family home with a 20% down payment decreased by 2.4% year-over-year in the third quarter.

In Santa Cruz County, the median price went from $975,000 in 2020 to approaching $1,200,000 today.

Housing clash involving two mortgage giants could drive up costs

The Trump administration's latest push to end government conservatorship of Fannie Mae and Freddie Mac has the housing world abuzz, according to Yahoo/Finance. According to the National Association of REALTORS, these government-sponsored enterprises (GSEs) guarantee about 70% of U.S. mortgages. Any alterations to their structure could send shock waves through the housing market, impacting everything from mortgage rates to affordability.

Fannie Mae and Freddie Mac have been under federal control since 2008 when the financial crisis pushed them into conservatorship. They are critical to the housing market because they buy mortgages from lenders, package them into securities and sell them to investors. This process allows banks to maintain the liquidity they need to continue issuing loans that help millions of Americans obtain long-term fixed-rate mortgages. Privatizing these two major lenders could remake the entire housing finance system. Advocates argue that it would reduce taxpayer risks and bring competition into the market. Critics, however, caution that it could come at a high price for borrowers. Without the implicit guarantee from the government, investors might grow more wary of mortgage-back securities, forcing up yields and, ultimately, mortgage rates. Time will tell!

C.A.R. market update as of 12/2/24

News on the economy and the housing market last week was mostly positive and encouraging.

There was also good news in the housing market, as conforming loan limits were raised for 2025 and mortgage rates continued to recover after reaching their recent peak in early November.

FHFA raises 2025 loan limits for California's housing markets

The Federal Housing Finance Agency (FHFA) has announced that the conforming loan limit (CLL) for one-unit properties will increase to $806,500 in 2025, marking a 5.2% rise from the 2024 limit. This adjustment reflects the 5.21% increase in average U.S. home values between the third quarters of 2023 and 2024, as indicated by the FHFA House Price Index.

In high-cost areas, where 115% of the local median home value surpasses the baseline CLL, the loan limit will be higher, with a new ceiling of $1,209,750 for one-unit properties. In California's high-cost areas, such as parts of the Bay Area, Los Angeles, and Orange County, the increased conforming loan limit for 2025 will help more homebuyers access government-backed mortgages. The new ceiling of $1,209,750 for one-unit properties allows buyers in these regions to secure financing without resorting to jumbo loans, which often come with higher interest rates and stricter qualification criteria. This adjustment reflects the state's consistently high home prices and provides greater affordability options for those navigating California's competitive real estate market. It is expected to benefit middle-income borrowers, particularly first-time homebuyers, by expanding access to loans under more favorable terms.

Court grants final approval of NAR's settlement agreement

Judge Stephen Bough last week granted final approval of the National Association of Realtors® (NAR) settlement agreement in the class action case related to broker commissions. The California Association of Realtors (C.A.R.) supports the judge's final approval as a reasonable and fair compromise that allows REALTORS® and REALTOR® organizations nationwide to move forward and serve consumers.

The agreement will resolve claims against NAR, over one million NAR members, all state/territorial and local REALTOR® associations, all association-owned MLSs, and all brokerages with an NAR member as principal that had a residential transaction volume in 2022 of $2 billion or less.

The judge's approval of the settlement is an important step, but not the final one. It's likely that many objectors will appeal the settlement to the Eighth Circuit Court of Appeals. While the outcome there may be unclear, the appellants would face an uphill battle in challenging the settlement and its approval.

Remember, sellers still have the choice of offering compensation to buyer brokers. And buyers will sign a written agreement with their agent before touring a home.

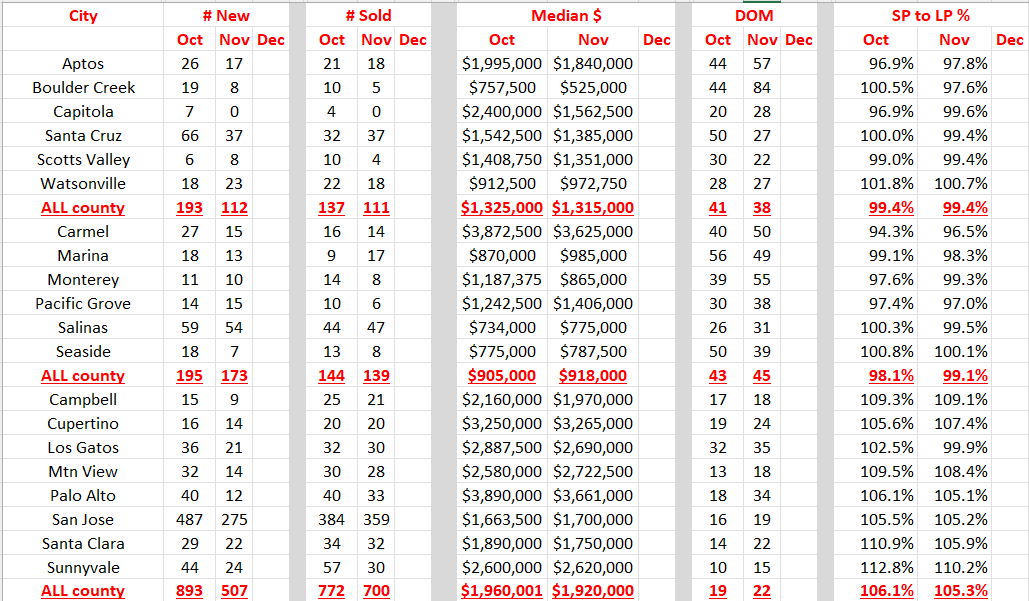

Oct/Nov stats for Santa Cruz, Monterey Counties & the Bay Area

Comments: Not much new to report here. It's November and this is what happens this time of year. New listings continued to decline month over month in all 3 counties and sales were down as well. The median price barely changed as did days on market and sale to list price ratio. Prices remain high as the lower than low inventory continues. (Display of MLS data is deemed reliable and is not guaranteed accurate by the MLS as of 10/31/24)