JANUARY 2023

What’s happening and what’s to come?

As sales decline, and new properties are hard to find, we are seeing a true slowdown in our market locally and in the Bay Area.

One indicator is the number of new listings coming on the market. As a comparison, in Santa Cruz County in 2022 for the October-November-December the numbers were (96-85-48) respectively as compared to 2021 which were (128-105-53). In Monterey County for 2022 it was (110-100-60) and in 2021 it was (200-145-106). In Santa Clara County for 2022 it was (576-418-243) and in 2021 it was (840-552-370). This decrease equates to a 19.9% decline annually in Santa Cruz, 40.1% decline in Monterey and 29.7% decline in Santa Clara. If this continues it will just add to the increasing short supply of available homes in California and a continuing housing crisis.

If you read the next article, you will see the National Association of Home Builders is stating builder confidence is the lowest confidence reading since mid-2012, with the exception of the onset of the pandemic in the spring of 2020. Builders are struggling to keep housing affordable for home buyers. The latest survey shows 62% of builders are using incentives to bolster sales, including providing mortgage rate buy-downs, paying points for buyers and offering price reductions. But with construction costs up more than 30% since inflation began to take off at the beginning of the year, there is little room for builders to cut prices.

As I keep you updated on the market, one can only hope things improve, inventories increase and prices level out so that all can enjoy the benefits of home ownership.

Builder confidence declined every month in 2022

High mortgage rates, elevated construction costs running well above the inflation rate and flagging consumer demand due to deteriorating affordability conditions have dragged builder sentiment down every month in 2022.

Builder confidence in the market for newly built single-family homes posted its 12th straight monthly decline in December, dropping two points to 31, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released today. This is the lowest confidence reading since mid-2012, with the exception of the onset of the pandemic in the spring of 2020.

Should you buy a home after 60?

According to Yahoo Finance, buying a home after age 60 may not necessarily be associated with retirement, but homeownership at any age can have a lasting impact on your retirement finances, such as the opportunity to build equity.

Depending on your circumstances, buying a home at an older age can be a blessing or curse. While you can reap tax advantages and leave a legacy for families, owning a home is a commitment with definite financial implications. Therefore, evaluating your financial capabilities and your plan for the next few decades can help you decide whether it’s best to put down your roots as a homeowner or become a renter with fewer responsibilities.

One third of Californians have no mortgage

According to the Orange County Register, California has 2.4 million households living what many consider a dream – being a free-and-clear homeowner, the third-highest count among the states, according to 2021 Census data. No-mortgage owners in California make up about 33% of all homeowners – and only four places have a smaller share: D.C. at 24%, Maryland at 28% and Colorado and Utah at 30%.

Census tracks the expenses owners incur for their shelter such as property taxes, insurance, routine operation and upkeep of the residence, and mortgage payments – or not, in the case of the free-and-clear crowd. Californians with no mortgage had a median monthly housing cost of $694 in 2021. For those Californians with a mortgage, their median monthly cost was $2,523 a month in 2021.

Typical monthly payment is nearly $300 less than October peak

According to Redfin, a combination of slowing price growth, lower mortgage payments and homes staying on the market longer is making the market a bit more favorable for buyers than in the fall, and some are starting to return.

Declining mortgage rates have cut nearly $300 from the typical homebuyers’ monthly housing payment since rates hit a peak of 7% in late October. That’s brought out a few buyers in the last few weeks as rates have fallen. Many people who were outbid on multiple homes during the buying boom are seizing this moment because they can take their time touring homes and negotiate on price and terms with sellers.

Home price increases post smallest gain in two years

Higher mortgage rates and consumer worries are hitting home prices, which are now 2.5% below the spring 2022 peak and are expected to continue to move lower this year, according to CoreLogic.

Home prices in November were still 8.6% higher than during the same month in 2021, but it was the first year-over-year reading in single digits in 21 months. It is also the lowest rate of appreciation since November 2020. CoreLogic forecasts price movement to fall into negative territory by spring before rebounding to about 2% to 3% growth in the fall.

Mortgage rates will dip below 6% soon

After doubling from a year ago, mortgage rates likely will settle below 6% and experience less volatility this year, predicts Nadia Evangelou, senior economist and director of forecasting at the National Association of REALTORS®. But we’re not there yet: The 30-year fixed-rate mortgage averaged 6.48% this week, according to Freddie Mac. “Although rates remain more than double a year ago, they will likely stabilize as inflation will continue to slow down in the coming months,” Evangelou says.

Until then, home buyers may be in wait-and-see mode. Affordability has been hammered by higher rates in recent months. Evangelou says the qualifying income for homeownership is now near the $100,000 threshold, which means only 32% of all households and 15% of all renters can afford to buy a median-priced home. The majority of these households are Gen Xers, whose median age is 51, she adds.

But many aspiring buyers from younger generations are still waiting to jump in. Home buyers are waiting for rates to decrease more significantly, and when they do, a strong job market and a large demographic tailwind of millennial renters will provide support to the purchase market. Moreover, if rates continue to decline, borrowers who purchased in the last year will have opportunities to refinance into lower rates.

Sales of luxury homes drop nationwide

According to Redfin, sales of luxury U.S. homes fell 38.1% year over year during the three months ending Nov. 30, 2022, the biggest decline on record. That outpaced the record 31.4% decline in sales of non-luxury homes. Redfin’s data goes back to 2012.

The luxury market and the overall housing market have lost momentum this year due to many of the same factors: inflation, relatively high interest rates, a sagging stock market and recession fears. But the high-end market has slowed at a sharper clip for a handful of reasons.

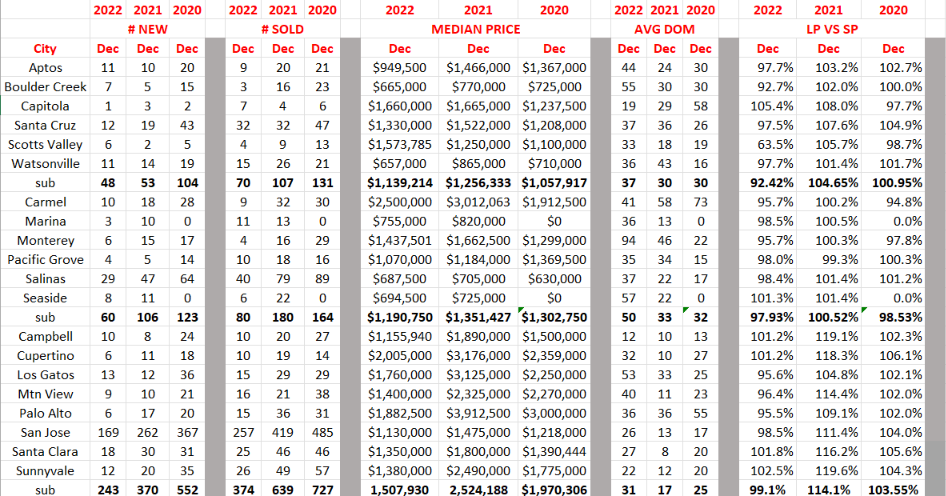

December market statistics for Santa Cruz, Monterey & the Bay Area

Comments: As one reviews this chart it shows a decline in new listings and sales for three straight years. What is unexpected is how steady median prices (although declining a bit) have been in Santa Cruz and Monterey counties. But look at Santa Clara County with an average decline in median price of 40% from 2021 and only a 21.9% increase over 2020. This truly shows luxury homes are showing a slowdown. Days on market can vary depending how many properties sold and at what price so not a true stat to follow. List price to sales price is following median price with a decline in 2022 over 2021 and a decline in 2020 over 2021. (Display of MLS data is deemed reliable but is not guaranteed accurate by the MLS)