MAY 2023

Should you rent or buy?

Buying a home has traditionally been seen as the smarter financial move. But with interest rates still high, the median mortgage payment has reached a record high of over $2,000 per month since 2009, according to the Mortgage Bankers Association.

In major cities like Boston, where the cost of homeownership has risen by more than 30% in the past year, it may be cheaper to rent instead of buy. Other cities where renting is less expensive than owning include Seattle, San Francisco and Austin, according to real estate website Realtor.com.

But the American dream of homeownership is being challenged by high home prices and mortgage rates, leading some to consider renting as a wiser option. According to a recent survey by the National Multifamily Housing Council, a public policy group, the monthly cost of owning a home is now an average of $1,000 more than renting.

According to a report by CBS News, housing experts also suggest setting a budget and sticking to it, even during a bidding war. Additionally, experts advise using the 28-36 rule, which means spending no more than 28% of your gross monthly income on housing and no more than 36% on all debts.

New mortgage rates explained by Fannie and Freddie

The Federal Housing Finance Agency (FHFA) implemented changes recently to the fee structure of conventional mortgages guaranteed by Fannie Mae and Freddie Mac, effectively lowering the fee gap between borrowers with high credit scores and those with low ones.

The change is part of a government initiative to make homeownership more affordable to underserved communities and first-time homebuyers, but critics say it disadvantages middle-income borrowers who are more financially prepared to buy a house - and less risky to lend to.

While low-income borrowers and those with credit scores below 680, as well as first-time homebuyers, will likely see lower monthly costs going forward, the changes could also make it harder for borrowers with good - but not great - credit and income to purchase a home. Fees also increased for borrowers who make larger down payments, those who apply for a cash-out refinance and those who buy a second home.

There are a number of variables at play, including individual borrowers' loan type and loan-to-value ratio. Under the new fee structure, a borrower with a 740 credit score and a 15% down payment would pay 1% in fees. On a $350,000 loan, that comes out to $3,500 on top of the loan balance. Under the previous fee schedule, the same borrower would pay a 0.2500 fee, or $875. FHFA fees, are referred to colloquially as "upfront fees," though in practice, their cost is usually baked into the interest rates homebuyers pay, and consequently, their mortgage payments. Homebuyers with good credit still pay less than "riskier" borrowers under the new structure.

Mortgage demand drops as rates dip

Mortgage demand from homebuyers has been erratic to say the least during the usually busy spring housing market, according to a report from CNBC.. That is likely because today's buyers are hypersensitive to mortgage rates, which have been fluctuating widely week to week but which are still considerably higher than they were a year ago. Now, several bank failures are starting to make it more difficult even for wealthier buyers.

Mortgage applications to purchase a home dropped 2% last week compared with the previous week, according to the Mortgage Bankers Association's seasonally adjusted index. Demand was 32% lower than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 6.50% from 6.55%, with points remaining at 0.63 (including the origination fee) for loans with a 20% down payment. The rate was 5.36% the same week one year ago.

The average rate for jumbo loans (higher-balance mortgages) was slightly lower at 6.37%, but that spread has been shrinking for the last few months. Jumbo loan rates had been far lower than conforming because banks generally hold these loans on their balance sheets, as Fannie Mae and Freddie Mac don't purchase them.

"The jumbo-conforming spread continues to narrow, an indication that there is reduced lender appetite for jumbo loans following the recent turmoil in the banking sector and heightened concerns about liquidity," wrote Joel Kan, MBA's deputy chief economist, in a release. "The spread was 13 basis points last week, after being as wide as 64 basis points in November 2022." Mortgage rates were volatile to start this week, with more concern over bank failures and a much-anticipated Federal Reserve meeting Wednesday.

U.S. commercial property market is in trouble

According to Charlie Munger, a VP at Berkshire Hathaway, there is trouble ahead for the U.S. commercial property market. The 99-year-old investor told the Financial Times that U.S. banks are packed with "bad loans" that will be vulnerable as "bad times come" and property prices fall. "It's not nearly as bad as it was in 2008," he told the Financial Times in an interview. "But trouble happens to banking just like trouble happens everywhere else."

Munger's warning comes as U.S. regulators have asked banks for their best and final takeover offers for First Republic by Sunday afternoon, the latest in what has been a tumultuous period for midsized U.S. banks. Since the failure of Silicon Valley Bank in March, attention has turned to First Republic as the weakest link in the American banking system. Shares of the bank sank 90% last month and then collapsed further this week after First Republic disclosed how dire its situation is.

Berkshire Hathaway has largely stayed on the fringe of the crisis despite its history of supporting American banks through times of turmoil. Munger, who is also Warren Buffett's longtime investment partner, suggested that Berkshire's restraint is partially due to risks that could emerge from banks' numerous commercial property loans.

"A lot of real estate isn't so good anymore," Munger said. "We have a lot of troubled office buildings, a lot of troubled shopping centers, a lot of troubled other properties. There's a lot of agony out there."

Market wrap-up according to C.A.R.

News from the end of April shows the economy continues to grow but doing so in a slower pace. The early reading for Gross domestic product (GDP) of the first quarter of this year suggests that the economy expanded but the momentum appeared to have fizzled out.

When looking at retail sales and personal spending, consumers had been holding back despite real income improving nine months in a row. While strong labor market continues to support wage growth, it also translates into higher labor costs and puts upward pressure on inflation. On top of that, recent bank failures added uncertainty to the overall health of the economy in the long-run and suppressed consumer confidence on the future expectation.

As for the real estate market, the short supply of existing homes for sale steered more home buying activity into the newly constructed housing sector, which comprised 33.2% of total single-family housing inventory in March - nearly double the 17.8% average in the year before the pandemic.

Consumer confidence falls as expectations about the future become uncertain: Consumer confidence dipped to a six-month low in April as growing concerns about the future and the stability of the banking system weigh on their sentiment. According to the Conference Board, the Consumer Confidence Index fell to 101.3 in April driven by a steep drop in the expectations component, which tumbled to 68.1 - the lowest reading since July.

The drop in the forward-looking measure, triggered by fears of what lays ahead, could be a sign of pull-back on consumer spending in the near future. Meanwhile, the present situation index rose slightly to 151.1 during the same month, as consumers remained upbeat about both the labor market and business conditions.

Consumers' reliance on credit and savings diminishes: The highest inflation in decades pushed consumers to rely on credit much more than in the past to sustain their spending. The six biggest increases in revolving credit in the last 20 years all occurred within the past 12 months. Credit is getting more expensive and more challenging to come by, however, as banks tighten up their credit standards due to recent bank failures.

Moreover, although the personal savings rate rose to 5.1%, the highest in over a year, households are still saving a lower share of income compared to pre-pandemic levels. That said, income is still the real driver for most recent spending, and the tight labor market continues to provide support on wage growth. With inflation receding, real disposable income continued to climb for now and nudged higher for the ninth consecutive month in March.

Vacant property scams

The U.S. Secret Service has observed an alarming increase in reports of real estate fraud associated with vacant and unencumbered property. Criminals are posing as owners of vacant land and contacting real estate agents to promptly list targeted properties, generally pushing for a cash sale under market value. Real estate agents have reported that the initial communication is generally unsolicited with a claim of an illness or financial hardship of the landowner.

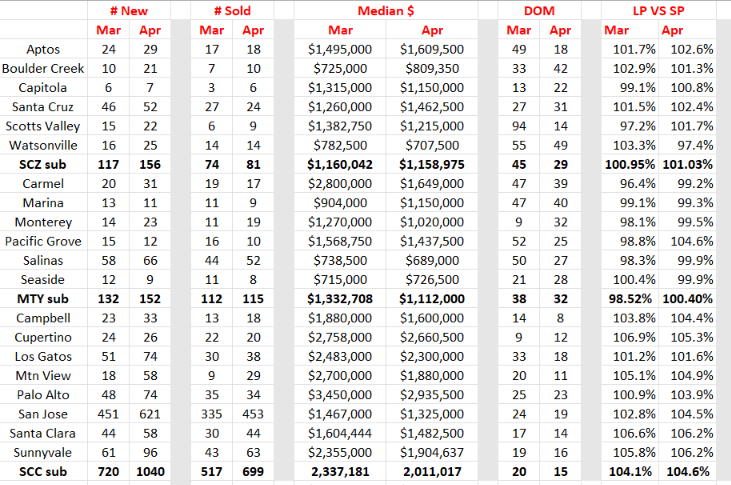

April 2023 stats for Santa Cruz, Monterey & the Bay Area

Comments: A very good report as compared to March and the beginning of 2023. New listings were up across all 3 counties, but sales were not up as much statistically. ie: 33% to 9.4% in SCZ, 15.1% to .02% in MTY and 44.4% to 35.2% in SCC. As for median price, it was down across the board and most noticeably in MTY at 16.5% and in SCC 13.9%. Days on the market was also down county wide and list to sales price remaining above 100% and increasing slightly in SCZ and SCC and over2% in MTY. These statistics are typical for this time of year and should last thru July. We shall see. (Display of MLS data is deemed reliable but is not guaranteed accurate by the MLS)