June 2022

Hot market could offer hope for buyers, sellers

According to MarketWatch, double-digit home price increases nationwide compared to last year and rising interest rates are dampening housing affordability by raising the average monthly payment 50% more than a year ago. Those rising costs are sidelining more hopeful home buyers.

But there are signs that the housing market could be slowing, which could put less pressure on home prices and offer hope for home sellers and buyers. For the fourth straight month, sales of brand-new homes dropped, reaching their lowest level since the pandemic. Existing-home sales also decreased in April, falling for the third consecutive month and down nearly 6% compared to a year ago, according to National Assn. of REALTORS® data. The drop in sales could offer less competition to buyers who are eager to jump in but keep getting beat out.

Check out these local sales stats in comparison over the last three years for May:

Many move-up buyers are leveraging newfound flexibility to employ creative strategies, such as relocating to an area offering homes that meet their family's needs without breaking their budgets. However, the shift to remote work is a double-edged sword: Working from home also explains over half of the 23.8% national increase in house prices between 2019 and November 2021, an economic study released last week concluded. That rise in house prices has pleased those homeowners who have been able and willing to sell, but it has also caused heartache for millions of first-time buyers who yearn to get a foot on the property ladder.

What's more, three-quarters of homeowners surveyed by Realtor.com who plan to sell their home in 2022 are also buying a home at the same time, which adds complexity to an already challenging task. While sellers stand to cash out record-high equity upon closing on their home, they are also facing higher prices and interest rates on their next home.

Homeowners accumulated $240,000 in equity over 10 years

As prices climb, homeowners who have owned their homes for a while have seen a boost in appreciation over the past decade. Homeowners in San Jose-Sunnyvale-Santa Clara, Calif.; San Francisco-Oakland-Hayward, Calif.; Anaheim-Santa Ana-Irvine, Calif.; and urban Honolulu, Hawaii built up the largest amount of home equity.

A homeowner who purchased a single-family existing home 10 years ago would have gained $229,400 in home equity if the home were sold at the median price in the fourth quarter of 2021, according to analysis by the National Association of REALTORS®. In the past five years, home prices have risen at an annual pace of nearly 10%. A homeowner who purchased a typical home five years ago would have gained $125,300 from just price appreciation alone.10%, NAR reports.

Sellers rush before market slows

Sharply higher mortgage rates have caused a sudden pullback in home sales, and now sellers are rushing to get in before the red-hot market cools off dramatically. The supply of homes for sale jumped 9% last week nationwide compared with the same period a year ago, according to Realtor.com. That is the biggest annual gain the company has recorded since it began tracking the metric in 2017. Real estate brokerage Redfin also reported that new listings rose nationwide nearly twice as fast in the four weeks ending May 15 as they did during the same period a year ago.

Check out these local new listing stats in comparison for the past two months:

Rising mortgage rates have caused the housing market to shift, and now home sellers are in a hurry to find a buyer before demand weakens further. Sellers clearly see the market softening. April sales of newly built homes, also measured by signed contracts, dropped a much wider-than-expected 16% compared with March. The list to sales price ratio has dropped over 3% in the Bay Area, which is a sign of things to come.

Mortgage rates ease but demand declines

Even after rates declined slightly last week, mortgage demand slipped to the lowest level since December 2018, according to the Mortgage Bankers Association. The average contract interest rate for a 30-year fixed-rate mortgage with conforming loan balances decreased to 5.33% for loans with 20% down. Application for a mortgage to purchase a home fell 1% last week compared with the previous week. Volume was 14% lower than the same week on year ago.

Weekly Market Update from the California Association of Realtors

The U.S. economy continues to show resilience despite growing challenges. Consumers have grown weary of the future, although their confidence level about their current situation was still solid by historical standards. Their expectations slipped along with their confidence in the economy though for the months ahead. Signs of momentum easing in the housing market continue to appear in recent weeks. Higher home prices and high interest rates have contributed to a fall in mortgage demand to the lowest level since the end of 2018, which if continue would be a concern for the real estate market. Existing homeowners, on the other hand, have benefited from the robust price gains and accumulated a record level of home equity collectively.

California Realtors work toward homeownership opportunities

One of the California Association of Realtors priorities has been to increase the allocation of funds in the state budget to homeownership. Last week, the Legislature released the Joint Legislative Budget Proposal which proposes to make a substantial investment in new affordable home construction, down payment assistance, and increased access to homeownership opportunities for all Californians.

C.A.R. along with a coalition of statewide organizations supports this Budget Proposal and pledges to work with the Legislature and Governor Newsom to make sure these investments are part of the final State Budget agreement. Specifically, we support the inclusion of:

The Legislature must pass a budget by June 15.

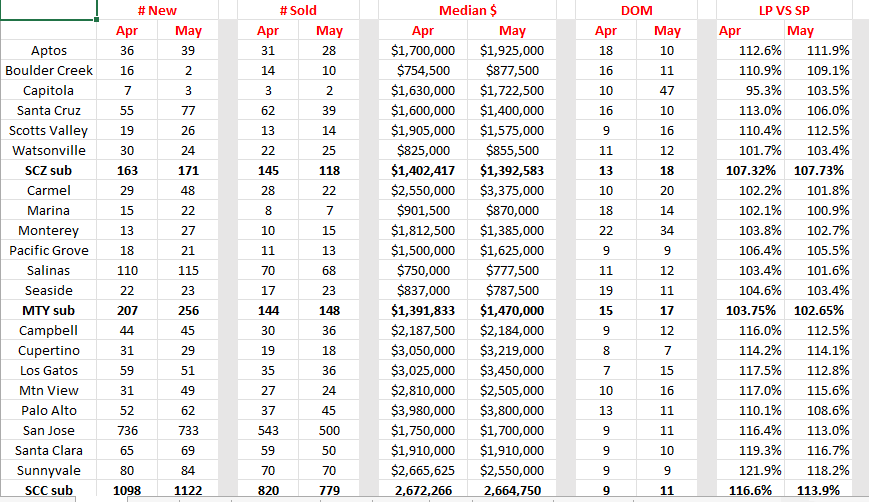

Apr-May Comparison Stats for Santa Cruz, Monterey & the Bay Area

And so, it begins as we are now seeing the decline in sales starting to happen. Obviously, some of these sales were in contract a month or two before and are now closing. I would think next month should see a significant reduction. New listings were up as sellers rush to capitalize before prices drop. The days on the market remained steady as inventory still remains low but the list to sales price decline shows sellers are negotiating and there may be good buys out there. One economist thinks we will see a recession in 2023, although it should not affect the housing market. Another one stated the stimulus made the recovery too fast as the unemployment rate was not expected to get to 5% for 6 years. I see the rise in interest rates only affecting the entry level, as the upper end has no problem buying at these prices. (Display of MLS data is deemed reliable but is not guaranteed accurate by the MLS)