JUNE 2023

The great out of California migration?

Based on county-level data released by the census earlier this year, except for Santa Cruz County, every county in the greater Bay Area had fewer residents in July 2022 than the previous year. The Bay Area and California both lost about 1% of their residents in the first year, and another .3% in 2022.

Of the nearly 500 cities or towns of any population in California for which the Census Bureau released data in May, Santa Cruz had the third-largest annual population change and is ranked as the second-fastest growing in the U.S. city at 12.5%, replacing Leander, Texas, which landed in the No. 2 spot last year.

That's second only to Georgetown, Texas, for the fastest growing city in the country, among those with at least 50,000 residents. "I don't think it's much of a mystery," said Santa Cruz Mayor Fred Keeley, "the University of California at Santa Cruz is the single largest entity in our town."

Since the beginning of time, humans have moved from one place to the next. Mass migrations like the Gold Rush of the 1800's and the Great Migration of the 1900's were led by populations motivated by historic events, urgent needs, opportunities, and tragedy. Similarly, COVID-19 was a catalyst for movement. According to U.S. Postal Service data, the pandemic increased relocations in 2020 by more than 94,000 compared with 2019.

Many recent moves have been anything but typical. The National Association of REALTORS®' 2022 Profile of Home Buyers and Sellers reported that the distance between the home buyers recently purchased and their previous residence, typically about 15 miles, jumped to 50 miles in 2022. Additional data showed that small towns and rural areas had the largest increase in homebuyer activity. What's driving the change?

Built to rent is transforming the landscape.

As home prices escalated, inventory shrank, and families sought more living space, communities of rental houses emerged as a growing option. Homeownership remains the overwhelming desire; in a recent survey, 74% of Americans called it a part of the American dream.

In the burgeoning build-to-rent and single-family rental niches, homes typically are new, resemble their for-sale counterparts, and offer a taste of homeownership without steep purchase prices, maintenance costs, real estate and school taxes, or homeowners association fees. Because the rents are comparable to traditional apartment leases of similar size and quality, they typically lease quickly—meaning they're helping to fill the country's huge housing shortage, estimated at 3.8 million homes by Freddie Mac in 2021.

Although the BTR trend started shortly before the pandemic, that "poured gasoline on the fire," says Michael Van Der Poel, managing partner at ACRE, a vertically integrated private equity firm that specializes in housing investment, including BTRs. People fled dense urban cores and crowded apartments for more space and greenery when unable to buy a house.

According to a National Association of Home Builders analysis of Census Bureau numbers, there were approximately 21,000 single-family BTR starts during the second quarter of 2022, a 91% increase compared to the second quarter a year before. Although many equate BTRs with three- or four-bedroom single-family homes, there's increasing variety as the trend evolves.

Who’s Renting

Homeownership remains the overwhelming desire of Americans. In a survey released by Bankrate last year, 74% of Americans called homeownership a part of the American dream. But the percentage was lower for younger adults, many of whom cited unaffordable prices, low inventory, and an inability to save for a down payment as barriers.

Millennials who can't afford to buy—or who aren’t ready to be tied to a location—aren't the only ones being targeted by BTR companies. They're also marketing to aging baby boomers, who might want to eliminate chores and costs, and to people hit by unexpected life changes, such as divorce or death, who want to gain an instant community.

Who's Behind the Trend

Developers and builders who have specialized in submarkets such as multifamily, active adult, senior housing, student housing and vacation homes are all dipping their toes into BTR to diversify their portfolios, since that segment represents a high-performance asset class offering faster lease-ups and lower turnover than apartments. Investors also see the wisdom of pumping in capital, sometimes through partnerships.

Locations

To date, locations that appeal are found in the "smile states," so named because of the smile shape they form, stretching through California, Arizona, Colorado, Texas, and the Southeast. These areas offer job growth; lower land, tax and living costs; good weather; and an influx of residents.

What They're Building

The average BTR community consists of 120 to 130 homes, but there's no single model. The sweet spot for many BTR builders is a 2,500-square foot detached home with three to four bedrooms, with renters prioritizing private outdoor space, the number of bedrooms and bathrooms, and a place for cars. But options in the market are expanding. On the smaller end, horizontal or "yard" homes, similar to garden-style apartments, may run less than 1,000 square feet.

When it comes to materials and furnishings, the goal is to mirror for-sale housing and Class A apartment buildings but tailor choices to each market. Common denominators are quartz or granite countertops, stainless steel appliances, luxury vinyl tile, smart thermostats and doorbells, strong Wi-Fi connectivity and fresh color palettes. Yardly includes doggie doors since approximately two-thirds of its residents own a dog.

Amenities

Another way some builders set themselves apart is by incorporating a clubhouse or other typical multifamily amenities. The industry debates how much these attract residents and improve developers' bottom lines. Wolfson's view is that if a company has a project that has capacity in the financial underwriting to do so, it should.

Price Points

Build-to-rent prices generally run slightly more than prices for apartments of a comparable size and quality. Wilkes has found that renters will pay a 10% to 20% premium, regardless of the market.

Wolfson's projects rent for between $2,500 and $3,500 monthly. Northmarq is involved with one development that features attached townhomes priced at $1,500 to $2,000 a month and single-family homes priced at $2,000 to $2,500 monthly. As the niche evolves, Walker thinks the price range will grow to reflect greater variety in size and amenities, similar to the for-sale and multiapartment markets with entry-level, move-up and luxury options.

Long-term Outlook

The question is whether developers, builders and investors will hold onto communities, sell them as an entity or piecemeal, or convert them to for-sale housing. One current strategy is to sell a community when lease-ups hit 90%, but it remains flexible as the real estate environment is ever-changing. Other take a long-term approach and believe strongly in the fundamentals that it hopes to retain communities "forever," yet is sensitive to market dynamics and potential disposition opportunities.

3 Dangers to look for in older homes.

Lead, asbestos, and mold can pose dangers when renovating or flipping older homes.

1. LEAD

2. ASBESTOS

3. MOLD

Service animal requirements in Fair Housing

The use of service animals has been one of the most contentious fair housing issues in recent years, mainly because of the growing use of animals in emotional-support situations. One case—involving a housing provider who said he didn't allow dogs, regardless of whether they were service animals—was recently sent back to district court by the U.S. Court of Appeals for the Ninth Circuit. At issue: whether language by an applicant that implies a disability constitutes the requisite evidence to make a housing provider aware the applicant actually has a disability.

The case: In July 2020, Ashley McClendon and Sarah Gailey applied to rent Peter Bresler's property. Bresler's rental advertisement included a "no dogs" policy. Nonetheless, Gailey asked for permission to bring McClendon's support animal, a 50-pound terrier mix named Tinkerbell. In an email, Bresler said the dog's size was a problem.

Although communications between Bresler and Gailey didn't detail McClendon's mental and physical impairments, Gailey said Tinkerbell was a "verified support animal." Her emails also referenced the Americans with Disabilities Act and noted the animal's presence would be a "reasonable accommodation." After Bresler denied the application, McClendon sued under the Fair Housing Act and California's Fair Employment and Housing Act, alleging disability discrimination and negligence.

The U.S. District Court for the Central District of California initially awarded summary judgment to Bresler, noting the email correspondence didn't indicate Bresler was aware McClendon had a disability. The court found descriptions of the dog as a registered and verified support animal merely amounted to assumption. McClendon appealed.

The ruling: The Ninth Circuit overturned the lower court ruling, noting that a prospective tenant "who requests accommodation(s) for a service animal need not affirmatively identify his or her disability to trigger Fair Housing Act protection." Statements like "I have a therapy animal" or "I have an assistance dog" should reasonably alert a housing provider, the court said. The suit has been remanded to the district court for a ruling on whether Bresler should have known of McClendon's disability status. The appeals court highlighted the applicants' use of phrases such as "reasonable accommodation," "discrimination" and "service dog" as potential evidence. The appeals court also reversed the judgment dismissing negligence claims. In the pending case, the plaintiff will have to prove Bresler reasonably should have known of her disability; a reasonable accommodation is necessary for her to enjoy the rental; and the defendant refused to accommodate her.

The takeaway: Discrimination based on disability status includes refusing to make reasonable accommodations so all tenants have equal opportunity to use the rental, so: Avoid blanket policies that could discriminate against those with protected characteristics; Pay attention to phrases like "reasonable accommodation" or references to the Americans with Disabilities Act, which could trigger duties to accommodate; Make sure to reasonably accommodate a prospective tenant.

State Farm and Allstate to stop selling home insurance in CA.

State Farm and Allstate have announced they will no longer sell new home insurance policies in California because of wildfire risks and an increase in construction costs. C.A.R. has created a fact sheet to help address some common questions you and your clients may have about how this will affect consumers.

The fact sheet explains that these two companies HAVE NOT left the California insurance market, the implications for prospective homebuyers, whether other insurance companies will follow, the primary problems in the California insurance market, resources for clients who have further questions and what C.A.R. is doing to address the issue. C.A.R. also is putting together additional information and will send to members in coming weeks.

Additionally, United Policyholders, a non-profit organization whose mission is to be a trustworthy and useful information resource and an effective voice for consumers of all types of insurance, is offering a free webinar on Friday, June 9, at 12 noon to help consumers find insurance in fire-prone areas.

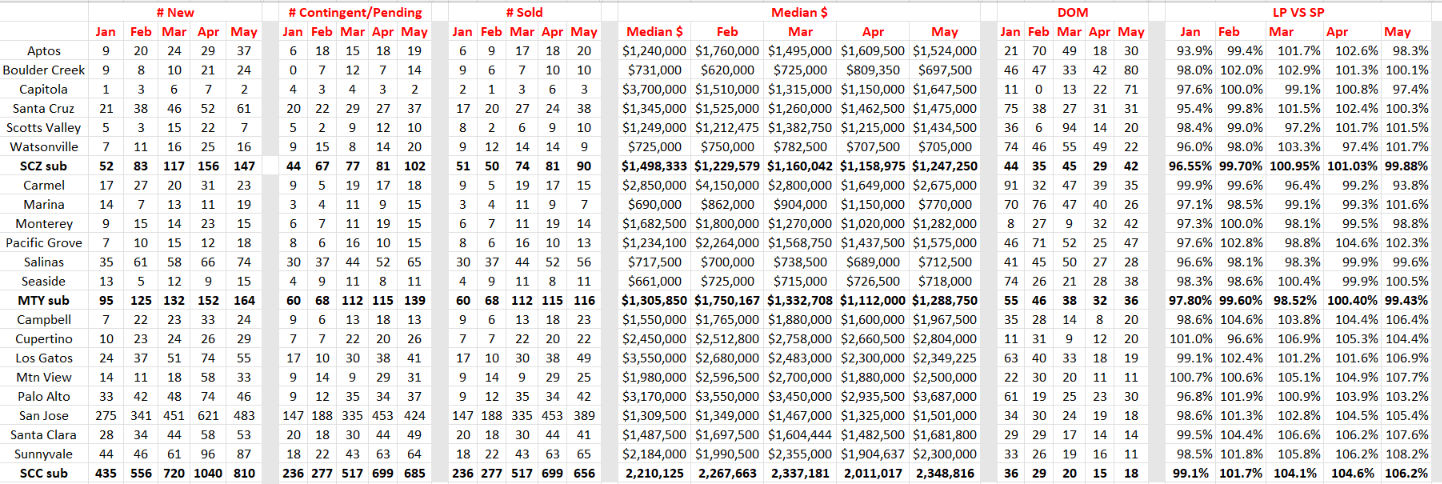

May 2023 stats for Santa Cruz, Monterey & the Bay Area

Comments: Well…the only thing that stands out to me is days on market (DOM). New listings were down up in Santa Cruz and Santa Clara after a 4-month increase. I added the category of contingent/pending to see if we could predict the future and it did. Those listings sold showed a meniscal increase and actually a decline in Santa Clara. Is this a sign of transactions cancelling? Median price is up again, so what else is new. The list to sales price ratio declined in 2of the 3 counties which is in line with the median price increasing. Still an uncertain market. (Display of MLS data is deemed reliable but is not guaranteed accurate by the MLS)