August 2020

Housing sector remains strong according to C.A.R.

The housing market remains one of the most solid sectors of the U.S. economy, with sales of new homes rising 13.8 percent nationwide in June. Demand from buyers continues to be robust, encouraged by another drop in mortgage rates, and as inventory tightens, more buyers are making concessions to win bidding wars. According to a Redfin survey, almost half of recent homebuyers made an offer sight-unseen.

Smaller markets are heating up as now-remote workers leave the big cities: Sacramento's housing forecast is stronger than most other metro areas in California, and Lake Tahoe real estate is moving at a record pace.

Is the pent-up demand for home unleashing the Economy?

The housing market was exceptionally strong at the beginning of 2020. In April, pending sales contracts hit their all-time lowest level during the most restrictive phase of the stay-at-home orders. Closing activity reached its bottom in May.

Since then homes that were listed then have drawn plenty of interest and prices have been rising at more than a 5% annualized clip. When the GDP contracted by 4.8% and consumer spending 8% respectively, the residential component from home sales, construction and remodeling activity grew by 21%. Has the importance of the home you live in been dramatically highlighted?

With the population social distancing, not going to the mall, not eating out, no vacations and no baseball, personal savings rose significantly. Government relief programs had implementation challenges but eventually provided generous levels of aid. The only major expense holding steady were fixed-rate mortgage payments and yet we saw a lowering of the interest rate.

Home sales nationally are forecast to be down only 11% in 2020, according to the National Association of Realtors, while prices should rise by 4%. In 2021, sales are expected to jump 15% while prices will grow 4-6%. The real question is whether the housing inventory will be there.

And what about the California market?

The real estate market continues to move, with nationwide sales of new houses jumping to a 13-year high and demand so high that buyers continue to make offers sight-unseen.

The CALIFORNIA ASSOCIATION OF REALTORS(R) released its June housing market report last week and it showed an unprecedented rebound in closed sales and the state also set a new all-time high price of more than $623,000.

After a record 41.4% decline in closed transactions in May 2020 due to coronavirus-related shelter in place orders, California saw the number of home sales rebound sharply in June. Home sales increased by more than 40% on a month to month basis and although California is still below 2019 levels by 12.8%, it is a marked improvement from April and May.

The percentage of California REALTORS(R) that had a transaction close escrow last week increased slightly to 26%. Low interest rates have been translating into increased demand for home showings and a trend of rising mortgage applications since mid-April although supply remains tight.

C.A.R.'s latest weekly analysis of MLS data across California reveals that pending sales in California have now been above their pre-coronavirus levels for 11 weeks in a row. Pending sales increased last week for the first time in nearly a month, this suggests that although July may see closed sales shoot back into positive territory, more robust growth in August and September remains very much in question as the pace of new escrows subsides.

One key reason the recent rebound is losing momentum in recent weeks is that there is not enough inventory on the market for buyers to purchase. (Haven't we been hearing this for the past three years or so?)

U.S. homeownership rate soars to a 12-year high

The U.S. homeownership rate soared to an almost 12-year high in the second quarter, according to Kathleen Howley a reporter with Housing Wire.

The homeownership rate jumped to 67.9%, the highest since 2008's third quarter, according to the Census Bureau. The homeownership rate for Black Americans rose to 47%, the highest since 2008, from 44%, the report said. A year ago, the rate for Black families was the lowest ever recorded. The rate for Hispanics increased to 51.4%, the highest in data going back to 1994, from 48.9%, the Census report said.

The cheapest financing costs on record have widened the pool of people who qualify for mortgages, said Lawrence Yun, chief economist for the National Association of Realtors. Lenders qualify applicants by the amount of the monthly payment measured against their income, and when financing costs go down the payment shrinks.

The average U.S. rate for a 30-year fixed mortgage fell to an all-time low of 2.98% in mid-July, breaking the 3% threshold for the first time, according to Freddie Mac data. Yun said he was expecting the homeownership rate to be higher because of the cheaper financing costs, but didn't foresee a jump of 2.6 percentage points that would put the number back to a level last seen before the widespread foreclosures that followed the 2008 financial crisis.

HUD Repeal of Fair Housing Rule Reverses Decades of Progress

The California Association of Realtors issued a statement 7/29/20 regarding HUD's announcement to end the 2015 Affirmatively Furthering Fair Housing (AFFHA) rule that will roll back provisions in the Fair Housing Act that encourage diversification and "foster inclusive communities."

"C.A.R. is reiterating and standing by its previous request for HUD to rescind its final rule on Affirmatively Furthering Fair Housing, which now opens the door for communities to increase segregation and deprive homeownership opportunities for many Americans," said C.A.R. President Jeanne Radsick. "We have spent many years trying to right decades of government-induced segregation and redlining; this rule would undo the last half-century of progress."

"Now is the time for HUD to work with the real estate community and fair housing advocates to draft a rule that will achieve greater homeownership opportunities for communities of color and fulfill the mission and spirit of the Fair Housing Act," said Radsick.

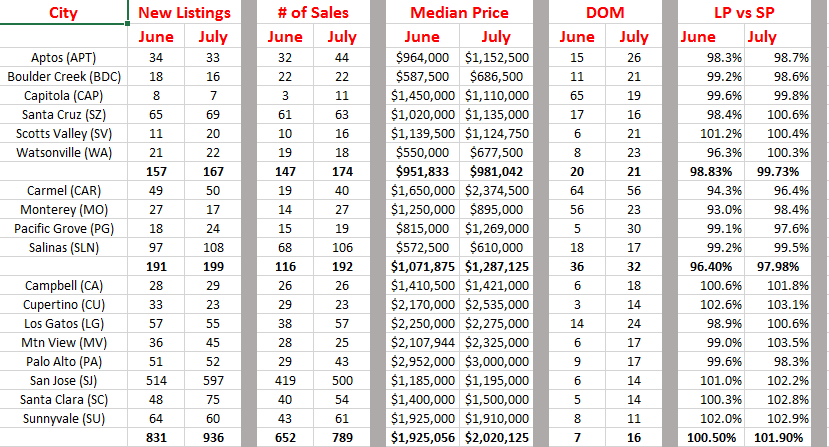

June to July Comparisons for Bay Area, Central Coast & Santa Cruz

Comments: Overall sales were up over new listings on average for all three Counties. Total sales in Monterey County showed the highest overall increase at 65%. All three Counties showed an uptick in Median Price but again Monterey County was up 20%. The Days on Market doubled in Santa Clara County and the list to sale price ratio increased in all three counties. Display of MLS data is deemed reliable but is not guaranteed accurate by the MLS.